Budget Process 2024

Developing the Annual Budget

Mesa County's budget process builds on several requirements established in State statute:

-

The budget must be balanced, meaning expenditures cannot exceed estimated revenues and fund balances

-

The County Administrator must propose a budget by October 15, and the Board of Commissioners must adopt a budget by December 15

-

The County must make the budget available and allow for public comment prior to adoption

The development of the annual budget begins with the development of budget requests by each department and elected official. In addition to estimating expenditures, revenues, and staffing needs, departments must identify their budget year goals, objectives, and performance indicators and submit information on how their funding requests support County-wide strategic initiatives. After departments complete their budget submissions, a Budget Review Team made up of senior leaders and fiscal managers from across the County evaluates each budget request, meets with every department to discuss their budget, and makes recommendations on funding and staffing levels. These recommendations form the basis of the proposed budget. After the County Administrator presents the proposed budget to the Board of Commissioners in public hearing, departments may appeal budget decisions directly to the Board. The Board makes final decisions on all appeals and may give additional direction prior to the budget being finalized. On December 1, the County Assessor publishes the Certification of Values and the County determines the mill levy for the budget year. The budget process concludes when the Board of Commissioners adopts and appropriates the budget, sets the mill levy, and establishes the authorized staffing level by resolution during public hearing.

Changes from the Proposed to Adopted Budget

The proposed budget represents the County's best estimates based on the information available at the time it is developed and presented, and staff generally strive to minimize changes to the budget prior to adoption. However, changes to the budget are often necessary as a result of new information, emergent needs or priorities, additional Board direction, and the identification of errors and omissions during peer review of the budget. For instance, since the County Assessor's final certification of property values is not available until December 1st each year, staff must wait to finalize property tax revenue estimates until well after the proposed budget is submitted.

Compare the adopted to the proposed budget using the figure below. You can also view a table detailing the changes made from the proposed to the adopted budget. 2023 Budget - Changes from Proposed to Adopted Budget.

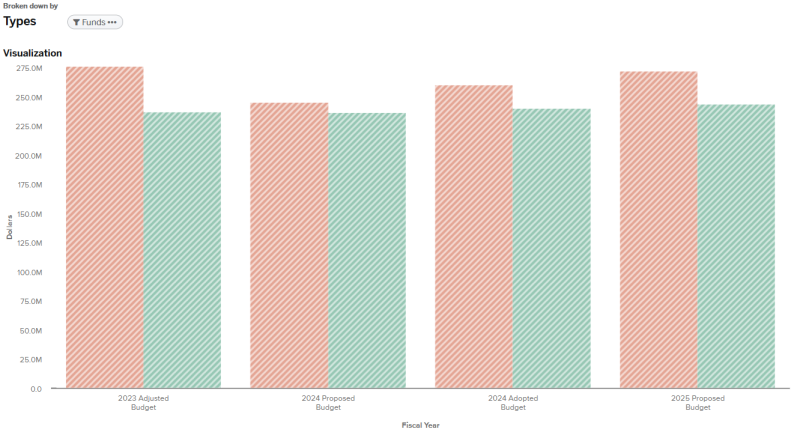

2024 Budget Milestones: All Funds

How did the budget for all funds change during the budget process?

| 2023 Adjusted Budget | 2024 Proposed Budget | 2024 Adopted Budget | 2025 Proposed Budget | |

|---|---|---|---|---|

| Revenues | $ 237,706,075 | $ 237,062,353 | $ 240,724,243 | $ 244,753,361 |

| Taxes | 95,284,718 | 101,325,910 | 99,533,711 | 105,403,457 |

| Intergovernmental | 92,759,468 | 84,464,997 | 89,511,390 | 74,631,065 |

| User Charges & Fees | 38,589,247 | 41,234,285 | 41,641,981 | 42,627,564 |

| Transfers | 4,110,488 | 3,610,539 | 3,610,539 | 14,371,485 |

| Other Sources | 6,435,054 | 5,389,322 | 5,389,322 | 4,913,230 |

| Interest | 527,100 | 1,037,300 | 1,037,300 | 2,806,560 |

| Expenses | 276,477,203 | 246,101,222 | 261,056,944 | 272,718,093 |

| Personnel | 103,847,361 | 111,240,253 | 111,922,016 | 120,377,122 |

| Capital | 87,883,701 | 51,703,263 | 65,015,441 | 47,772,418 |

| Operating | 50,827,220 | 51,456,943 | 51,745,284 | 52,529,051 |

| Other | 27,757,644 | 26,617,925 | 26,791,364 | 24,005,971 |

| Transfers | 4,937,877 | 3,860,238 | 4,360,239 | 26,246,336 |

| Debt Service | 1,223,400 | 1,222,600 | 1,222,600 | 1,787,195 |

| Revenues Less Expenses | $ -38,771,128 | $ -9,038,869 | $ -20,332,701 | $ -27,964,732 |

2024 Budget Milestones: General Fund

How did the budget for the General Fund change during the budget process?

| Collapse All | 2023 Adjusted Budget | 2024 Proposed Budget | 2024 Adopted Budget | 2025 Proposed Budget |

|---|---|---|---|---|

| Revenues | $ 87,688,043 | $ 89,427,571 | $ 87,960,948 | $ 92,328,049 |

| Taxes | 46,467,005 | 50,107,392 | 48,514,091 | 51,787,454 |

| Intergovernmental | 26,107,242 | 24,901,500 | 25,028,178 | 24,812,428 |

| User Charges & Fees | 10,949,434 | 10,052,135 | 10,052,135 | 10,166,493 |

| Other Sources | 2,883,363 | 2,283,959 | 2,283,959 | 1,989,174 |

| Interest | 516,000 | 1,000,000 | 1,000,000 | 2,500,000 |

| Transfers | 765,000 | 1,082,585 | 1,082,585 | 1,072,500 |

| Expenses | 84,669,748 | 90,306,094 | 91,115,018 | 97,948,032 |

| Personnel | 51,438,069 | 57,111,583 | 57,634,018 | 62,698,101 |

| Operating | 26,592,101 | 28,827,125 | 28,940,925 | 29,890,983 |

| Other | 4,297,781 | 2,877,592 | 3,050,281 | 2,299,281 |

| Transfers | 1,951,677 | 1,120,596 | 1,120,596 | 2,795,720 |

| Capital | 390,120 | 369,198 | 369,198 | 263,947 |

| Revenues Less Expenses | $ 3,018,295 | $ -878,523 | $ -3,154,070 | $ -5,619,983 |

Amending the Budget

Colorado State Statute prohibits any expenditure in excess of annual appropriations. However, during the year amendments to the budget may become necessary due to unforeseen circumstances. The Board of County Commissioners may approve amendments to the budget in the following instances:

- To adjust the appropriation for an elected office,

- To adjust the appropriation for a fund, such as when it receives unanticipated revenues, or

- To transfer monies from one fund to another.

Transfers from one line-time account to another within the same department and fund, or among non-elected departments in the same fund, do not require Board approval.